Simulating Auditor Behavior: Building Checklists That Match Real Audit Flows

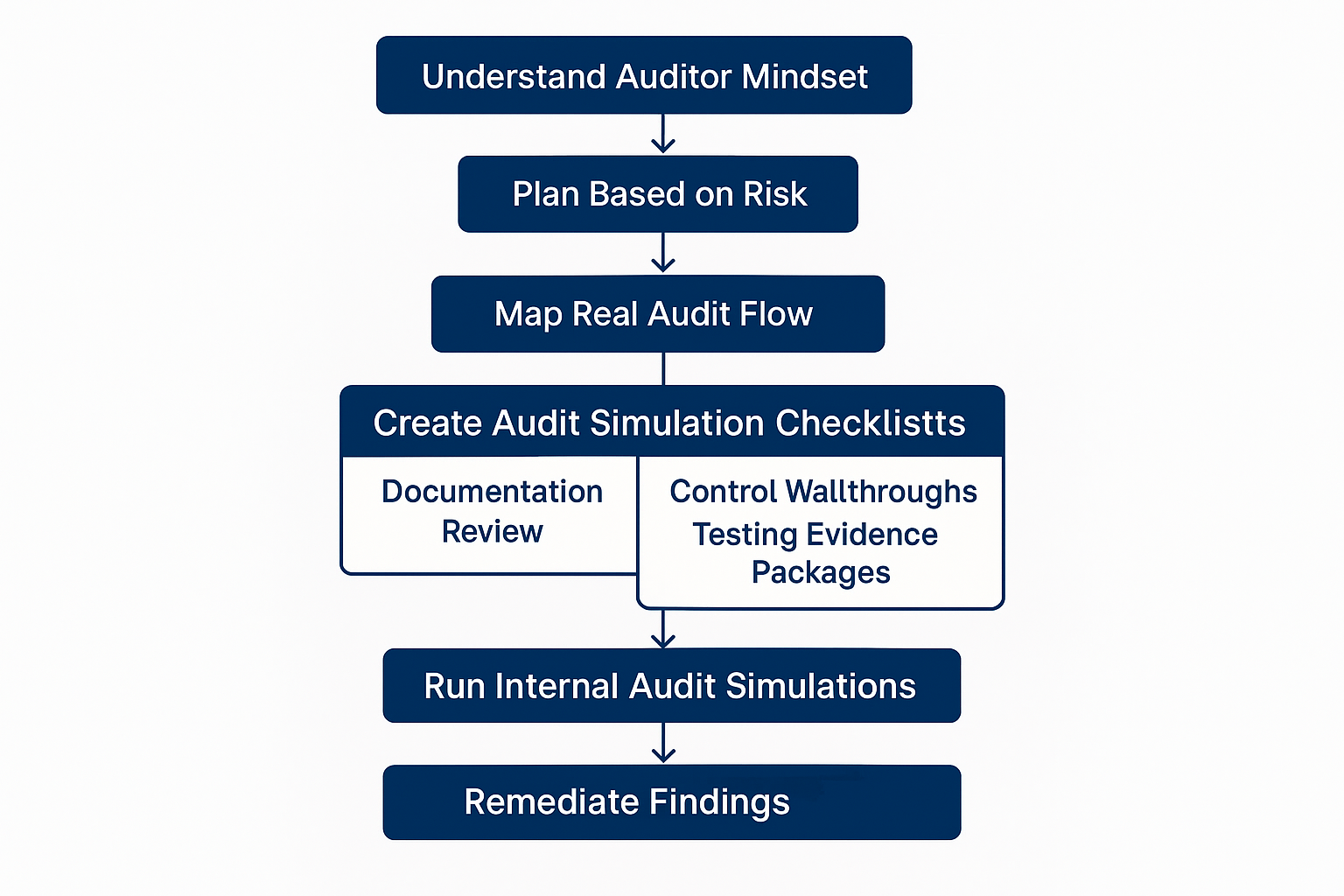

Understanding how auditors think and work is essential for organizations preparing for compliance reviews. By simulating auditor behavior and creating checklists that mirror real audit flows, companies can identify gaps before the actual audit begins, streamline their preparation process, and significantly improve their audit outcomes.

Understanding Auditor Behavior and Methodology

Auditors follow systematic, risk-based approaches when conducting reviews. They don't randomly examine documents or processes. Instead, they employ structured methodologies that prioritize high-risk areas and follow logical progressions through an organization's systems and controls.

Key characteristics of auditor behavior include:

Risk-based thinking drives every audit decision. Auditors assess which areas pose the greatest compliance risks and allocate their time accordingly. They look for patterns and anomalies that might indicate systemic issues rather than isolated incidents. Auditors also rely heavily on evidence trails, following documentation from source to conclusion to verify that controls function as described.

Professional skepticism is another defining trait. Auditors question assumptions and verify claims independently rather than accepting explanations at face value. This doesn't mean they're adversarial, but they maintain objectivity throughout the process.

The Anatomy of Real Audit Flows

Real audit flows typically follow a predictable structure that moves from understanding to testing to conclusion. This framework remains consistent across different audit types, whether financial, IT, operational, or compliance-focused.

Planning Phase Flow

The audit begins long before auditors arrive on-site. During planning, auditors review previous audit reports, analyze organizational changes since the last review, and identify new regulatory requirements that apply. They develop an audit plan that outlines scope, timing, and resource allocation based on their risk assessment.

Fieldwork Phase Flow

Once fieldwork begins, auditors follow a systematic progression. They typically start with walkthroughs to understand processes as they actually operate, not just as documented. This involves interviewing process owners, observing procedures in action, and tracing sample transactions through the entire workflow.

Next comes control testing, where auditors select samples and verify that controls operated effectively throughout the audit period. They examine supporting documentation, test system configurations, and validate that segregation of duties exists. For each control, they document their testing methodology, sample selection criteria, findings, and conclusions.

Reporting Phase Flow

The final phase involves synthesizing findings, discussing them with management, and issuing formal reports. Auditors categorize issues by severity, provide root cause analysis, and recommend corrective actions with reasonable timelines.

Effective audit preparation checklists don't simply list requirements. They replicate the auditor's thinking process and workflow, helping organizations see their controls through an auditor's eyes.

Designing Risk-Based Checklists

Start by categorizing items based on audit risk levels rather than alphabetically or by department. High-risk areas should appear first in your checklist, mirroring how auditors allocate their attention. For each area, include questions that an auditor would ask, not just yes/no compliance questions.

For example, instead of "Do you have an access control policy?" ask "How do you ensure that access rights are reviewed quarterly, and what evidence demonstrates this review occurred for the last four quarters?" This second question matches how auditors think about evidence and effectiveness.

Structuring Checklists by Audit Phase

Organize your checklists to match the phases auditors follow. Create separate sections for documentation review, control walkthrough verification, and testing evidence. This structure helps your team prepare materials in the sequence auditors will request them.

Documentation Review Section:Include items like policy documents with version control and approval signatures, organizational charts showing reporting relationships and segregation of duties, previous audit reports with management responses and remediation evidence, and process narratives that explain how procedures work in practice.

Control Walkthrough Section:Prepare for process demonstrations with clear process flows, identify key personnel for interviews, gather sample transactions that illustrate normal operations, and document exception handling procedures.

Testing Evidence Section:Compile logs and reports covering the full audit period, prepare access reports showing user provisioning and deprovisioning, organize change management documentation chronologically, and create evidence packages that link controls to supporting proof.

Simulating Common Auditor Testing Approaches

Auditors use specific testing techniques repeatedly. By understanding and simulating these approaches, you can pre-test your own controls using the same methods auditors will employ.

Sample Selection Simulation

Auditors rarely test every transaction. They select samples using statistical methods or judgmental approaches. Simulate this by randomly selecting 25-30 items from different time periods within the audit scope. Test these samples as if you were the auditor, looking for missing documentation, approval gaps, or timing issues.

Inquiry and Observation Techniques

Auditors interview multiple people about the same process to identify inconsistencies. Simulate this by having someone unfamiliar with a process interview the process owner, then interview someone who executes the process daily. Compare the responses. Discrepancies signal areas where documented procedures may not match reality.

Analytical Review Methods

Auditors compare current period data to prior periods, budgets, or industry benchmarks to identify unusual fluctuations. Build similar analytical reviews into your checklist. If metrics have changed significantly, prepare explanations with supporting evidence before the auditor asks.

Creating Evidence Packages That Meet Audit Standards

Auditors evaluate evidence based on specific quality criteria. Understanding these standards allows you to prepare documentation that satisfies audit requirements the first time.

Evidence Quality Characteristics

Effective audit evidence possesses several key qualities. It must be relevant to the specific control being tested, sufficient in quantity to support conclusions, and reliable in terms of source and creation method. Evidence created independently outside your organization carries more weight than internally generated documents.

Evidence Organization Best Practices

Create evidence folders organized by control objective rather than by document type. For each control, include a cover sheet that identifies the control description, testing period, preparer and reviewer, and links to supporting evidence. Number all pages consecutively and cross-reference related documents.

Prepare evidence indices that list what's included, where auditors can find it, and what each document proves. This approach demonstrates control over your documentation and reduces back-and-forth requests during the audit.

Incorporating Auditor Communication Patterns

How auditors communicate provides insights into their priorities and concerns. Building these communication patterns into your preparation improves your response quality.

Request List Anticipation

Auditors typically submit document requests in waves. The initial request is broad, covering foundational documents like policies and organizational structures. Subsequent requests become more specific, drilling into areas where initial reviews raised questions.

Create a staged preparation approach that mirrors this pattern. Prepare your foundation documents first, ensuring they're complete and current. Then anticipate follow-up questions based on gaps or ambiguities in those documents and prepare supplementary materials proactively.

Issue Discussion Frameworks

When auditors identify potential findings, they discuss them with management before finalizing reports. These discussions follow a predictable format: describing the condition observed, explaining the criteria or requirement, analyzing the cause of the gap, assessing the effect or risk, and discussing management's response.

Prepare for these discussions by conducting internal reviews using this same framework. When you identify issues during self-assessment, document them using this structure. This preparation enables more productive discussions with auditors and demonstrates management's commitment to addressing concerns.

Leveraging Technology to Simulate Audit Flows

Modern audit preparation increasingly relies on technology to simulate auditor behavior and automate checklist management.

Automated Control Testing Tools

Many organizations now use continuous control monitoring tools that automatically test controls and alert management to failures. These tools simulate auditor testing by running the same queries and analyses auditors would perform, but on a continuous basis rather than annually.

For example, segregation of duties monitoring tools automatically flag when users gain conflicting access rights, mirroring the access reviews auditors conduct during IT audits. Similarly, automated policy attestation systems track whether required acknowledgments occur, providing the evidence trail auditors seek.

Workflow Simulation Software

Some organizations build workflow simulation tools that map their processes and automatically identify control gaps. These tools analyze process flows, identify where controls should exist based on risk factors, and flag areas where controls are missing or inadequate.

This approach helps organizations see their processes through an auditor's risk-based lens, identifying vulnerabilities before they become audit findings.

Common Pitfalls in Checklist Design

Even well-intentioned audit preparation checklists can fail if they don't truly reflect auditor thinking. Several common mistakes undermine checklist effectiveness.

Checkbox Compliance Mentality

The most frequent mistake is creating checklists that focus on having policies and procedures rather than on proving they work. Auditors care less about what's written and more about what's actually happening. Your checklist should verify effectiveness, not just existence.

Instead of "Access control policy exists," your checklist should ask "What evidence demonstrates that access reviews occurred quarterly as required by the policy, and how do you know unauthorized access was promptly removed?"

Ignoring the Evidence Trail

Many checklists fail to address evidence quality and completeness. They confirm activities occurred but don't verify that proof exists in an audit-acceptable form. Each checklist item should include evidence requirements that specify what documentation must exist, how it should be dated and approved, where it's stored, and who can produce it quickly during the audit.

Static Rather Than Dynamic Approaches

Business environments change constantly, but many checklists remain static. Auditors adjust their focus based on organizational changes, new regulations, and emerging risks. Your checklist should similarly evolve based on recent incidents, system implementations, regulatory updates, and changes in key personnel or processes.

Implementing a Continuous Audit Readiness Mindset

The most sophisticated organizations move beyond periodic audit preparation to continuous audit readiness. This approach treats audit preparation as an ongoing process rather than a quarterly scramble.

Building Audit Thinking Into Daily Operations

Train process owners to think like auditors by asking them to regularly consider what evidence an auditor would request for their area, how they would explain process deviations, whether their documentation would satisfy audit standards, and what risks an auditor would identify in their processes.

This cultural shift transforms audit preparation from a compliance burden to a quality improvement opportunity. When employees habitually think about evidence and effectiveness, they naturally maintain audit-ready documentation.

Establishing Internal Audit Simulation Programs

Leading organizations conduct internal audit simulations using external consultants or internal audit teams. These simulations follow the same methodology external auditors use, providing realistic preparation experiences without the stakes of an actual audit.

Document findings from these simulations in the same format as real audit reports. Track remediation efforts and verify fixes before the next simulation or real audit. This iterative approach continuously improves your control environment and audit preparedness.

Measuring Checklist Effectiveness

How do you know if your audit simulation checklists actually work? Several metrics indicate effectiveness and help you refine your approach over time.

Pre-Audit Self-Assessment Results

Track the issues you identify through self-assessment versus those auditors find. If your checklist is effective, you should discover most issues before auditors do. A low ratio of auditor-identified to self-identified issues indicates your checklist accurately simulates auditor behavior.

Audit Efficiency Metrics

Measure how quickly you can respond to auditor requests. The time required to produce requested documents and the number of follow-up requests from auditors both indicate preparation quality. Well-designed checklists reduce both response times and follow-up requests.

Finding Severity Trends

Monitor whether audit findings are decreasing in severity over time. Effective checklists should help you address high-risk issues proactively, leading to fewer critical or significant findings and more low-risk observations over successive audits.

Conclusion

Simulating auditor behavior through well-designed checklists transforms audit preparation from a reactive, stressful exercise into a proactive quality improvement process. By understanding how auditors think, structuring checklists to match real audit flows, and building continuous audit readiness into daily operations, organizations can significantly improve their audit outcomes while strengthening their control environments.

The key is moving beyond superficial compliance to truly seeing your organization through an auditor's eyes. When your checklists ask the hard questions auditors will ask, demand the same evidence quality auditors require, and follow the same risk-based logic auditors employ, you're no longer just preparing for an audit. You're operating at a higher standard of control effectiveness that benefits your organization regardless of external reviews.

Effective audit simulation doesn't eliminate findings entirely, but it changes their nature. Instead of discovering critical control failures during the audit, you identify and address them beforehand. The audit becomes a confirmation of your control environment's strength rather than a discovery of its weaknesses, fundamentally changing the audit experience for everyone involved.

What’s a Rich Text element?

The rich text element allows you to create and format headings, paragraphs, blockquotes, images, and video all in one place instead of having to add and format them individually. Just double-click and easily create content.

A rich text element can be used with static or dynamic content. For static content, just drop it into any page and begin editing. For dynamic content, add a rich text field to any collection and then connect a rich text element to that field in the settings panel. Voila!

Headings, paragraphs, blockquotes, figures, images, and figure captions can all be styled after a class is added to the rich text element using the "When inside of" nested selector system.

Follow-up: Conduct a follow-up review to ensure that the remediation steps were effective and that the smart contract is now secure.

Follow-up: Conduct a follow-up review to ensure that the remediation steps were effective and that the smart contract is now secure.

In Brief

Remitano suffered a $2.7M loss due to a private key compromise.

GAMBL’s recommendation system was exploited.

DAppSocial lost $530K due to a logic vulnerability.

Rocketswap’s private keys were inadvertently deployed on the server.

Hacks

Hacks Analysis

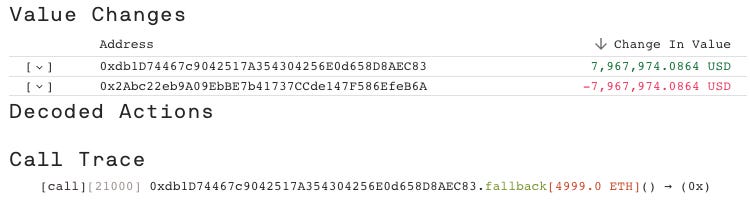

Huobi | Amount Lost: $8M

On September 24th, the Huobi Global exploit on the Ethereum Mainnet resulted in a $8 million loss due to the compromise of private keys. The attacker executed the attack in a single transaction by sending 4,999 ETH to a malicious contract. The attacker then created a second malicious contract and transferred 1,001 ETH to this new contract. Huobi has since confirmed that they have identified the attacker and has extended an offer of a 5% white hat bounty reward if the funds are returned to the exchange.